Healthcare Insurance as an Equity

Example of Healthcare Investment Plan (HIP):

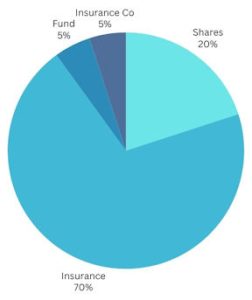

Family income $60,000 per year with a $500 per month insurance policy.

- 20%: $100 to purchase shares in the insurance company portfolio

- 70%: $350 medical coverage

- 5%: $25 for catastrophic fund

- 5%: $25 goes to insurance company

Tax Credits:

Insurance company matches the $100 to increase buyer’s stock purchasing power and receives a $100 tax credit.

97% distribution received by buyer.

- Income for more stock purchasing power.

- May be tax deferred or immediate capital gains tax income for the government.

- May use to pay premiums.

- May use to cover deductibles.

- Strengthen catastrophic funds.

The other 3%:

- 1/3 to insurance company for managerial fees.

- 2/3 funds health insurance for people below the poverty level.

- This 3% becomes a tax credit to the buyer

Examples of insurance purchase and deductibles:

Cost of Insurance Plan Deductible

$50 $10,000

$100 $ 8,000

$500 $ 6,000

$1,500 $ 3,500

$2,000 $ 2,500

$3,000 $ 1,200

Above are examples. In general, buyer purchasing higher premiums has higher share purchasing strength and lower deductible. This encourages the purchase of the higher premium policies. The stronger an insurance’s portfolio and medical coverage attracts the purchase of plans with higher premiums.

The insurance companies that have strong returns and medical coverage spawn competition between them. Those that are less investment worthy with poor medical coverage and reimbursements will improve to heighten power of buyer’s investment and medical healthcare dollar and cost containment or they dissolve.